What Is a Defined Contribution Retirement Plan (and Why Should You Care)?

Many people already have at least a basic familiarity with defined contribution retirement plans without even realizing it.

Don’t believe me? Think about your 401(k) or traditional profit-sharing plan - those are two of the most common types and you must’ve heard of at least one of those!

Understanding the key features of defined contribution plans, along with the major sub-types within the defined contribution category, is critical for properly planning for retirement and maximizing the benefits offered by your employer.

This article will refresh the fundamentals of defined contribution plans, explain the difference between the two main categories within them (profit-sharing plans and pension plans) and give a brief overview of the primary plan types within each category so you can navigate retirement plans just a bit better.

Let’s start from the top.

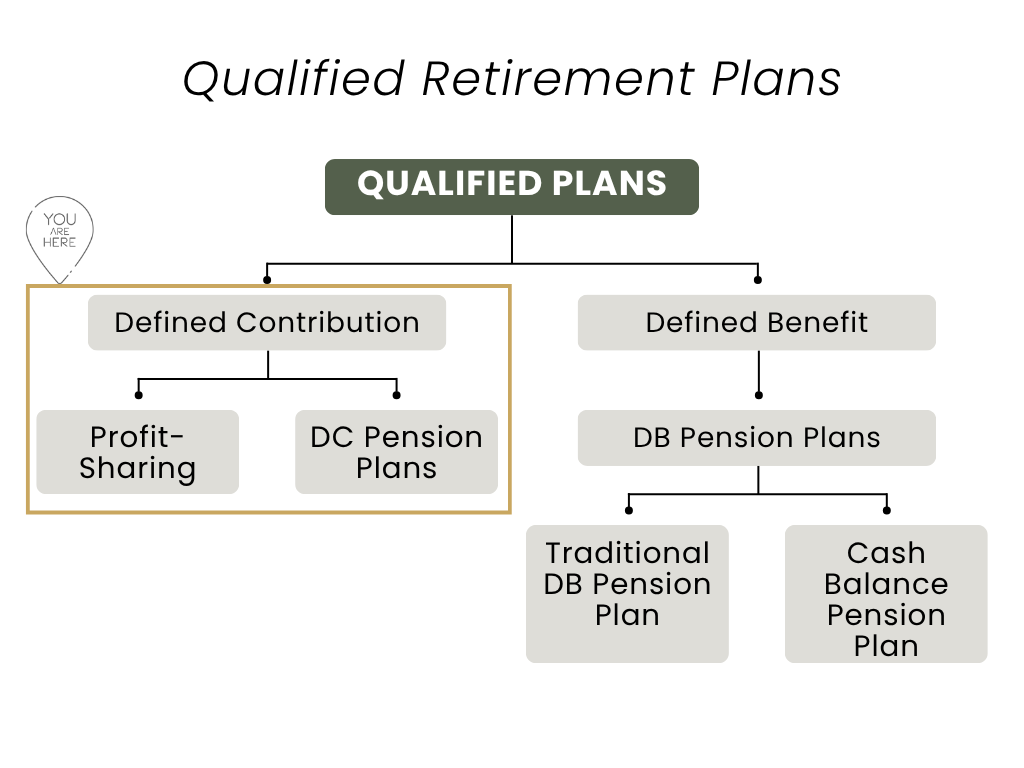

Defined Contribution Plans: A Quick Refresher

There are two primary types of qualified retirement plans:

Defined Contribution Plans

Defined Benefit Plans

Defined contribution plans focus on what is contributed into the retirement account during a given year rather than guaranteeing a specific retirement payout in the future.

Within the broader category of defined contribution plans, there are two major subcategories:

Profit-Sharing Plans

Pension Plans

(For a broader overview of qualified retirement plans and how they work, see our companion article covering qualified plans in simple terms.)

Defined contribution profit-sharing plans generally allow employers to make discretionary contributions to employee retirement accounts based on company profits or other formulas determined by the employer. The calculation of the amount is usually outlined in what's called the Plan Documents.

There are three major types of defined contribution profit-sharing plans:

Traditional Profit-Sharing Plans

Section 401(k) Plans

Employee Stock Ownership Plans (ESOPs)

The underlying concept behind many of these plans is that tying employee retirement benefits to company performance may help incentivize stronger employee performance and retention (or attract new talent).

Defined contribution pension plans, on the other hand, require employers to contribute to employee retirement accounts based on a predetermined formula. These plans are less common today but can still provide substantial retirement benefits when offered.

One important concept to remember with any Defined Contribution Plan: regardless of the type of defined contribution plan, the employee ultimately bears responsibility for the final retirement account balance because no specific retirement benefit or payout is guaranteed.

Defined Contribution: Profit-Sharing Plans

-

A traditional profit-sharing plan gives employers flexibility in how they contribute a portion of company profits toward employee retirement savings.

One of the major advantages of this type of plan for employers is flexibility. Contributions may be:

Fixed according to a formula

Variable from year to year

Completely discretionary

Suspended in certain years if needed

Generally, employer contributions are made annually or quarterly.

The funds contributed by the employer are deposited into individual employee retirement accounts and are generally not accessible until retirement or separation from service (subject to vesting and plan rules).

-

A Section 401(k) plan, more commonly referred to simply as a “401(k)”, is the most common qualified retirement plan in the United States.

Unlike some other profit-sharing plans, both employees and employers may contribute to a 401(k) plan.

One of the defining characteristics of a 401(k) is that employees are typically allowed to direct how their retirement funds are invested, often selecting among mutual funds, index funds, target-date funds, company stock, or other investment options offered within the plan.

This investment component is one of the major appeals of the 401(k), since account growth depends heavily on long-term investment performance.

Many 401(k) plans also include a profit-sharing feature that allows employers to make additional discretionary contributions to employee accounts beyond employee salary deferrals (employee salary deferrals is just a fancy way of saying the amounts the employee contributes). Importantly, however, employers are generally not required to make these discretionary profit-sharing contributions every year.

Like other qualified retirement plans, annual contribution limits apply to both employee and employer contributions, and these limits are generally adjusted annually for inflation.

The 401(k) itself contains many additional features and rules which include Roth options, matching contributions, vesting schedules, hardship withdrawals, and loans. All 401(k) plan features will be covered in a future article in more detail. For now, the key takeaway is understanding where the 401(k) fits within the broader framework of qualified retirement plans.

-

An Employee Stock Ownership Plan (ESOP) is a retirement plan in which employees receive ownership interests in the company, typically in the form of company stock rather than cash contributions.

The company determines whether and how much stock to contribute, often based on factors such as:

Company profitability

Employee compensation

Years of service

Individual performance

Over time, employees accumulate vested shares within their ESOP accounts. Upon retirement or separation from the company, employees may receive either:

The actual shares of stock, or

The cash value of those shares

There are several different forms of ESOPs, each with unique rules regarding vesting, distributions, diversification, and withdrawals.

Because ESOPs can result in employees holding significant amounts of company stock, participants should understand both the potential upside and the concentration risk associated with owning too much of a single company’s stock within their retirement portfolio.

Defined Contribution: Pension Plans

-

A Money Purchase Pension Plan (MPPP) is a defined contribution pension plan in which the employer is required to make contributions every single year.

The contribution amount is established in the plan document and is typically based on a fixed percentage of employee compensation.

Unlike discretionary profit-sharing plans, employer contributions to an MPPP are mandatory.

Another important characteristic of MPPPs is that no more than 10% of plan assets may generally be invested in employer stock. Additionally, these plans are entirely employer-funded, meaning employees do not contribute to the plan themselves.

Because of the pension structure and regulatory rules surrounding these plans, withdrawals are typically restricted until retirement age, commonly age 62 or later depending on the plan terms.

-

A Target Benefit Pension Plan combines features of both a Money Purchase Pension Plan and a traditional defined benefit pension plan.

When the plan is established, actuaries calculate the annual contribution amounts necessary to help participants reach a projected or “target” retirement benefit amount.

Typically, the target benefit is based on factors such as:

The employee’s age when entering the plan

Compensation levels

Expected years until retirement

The employer is then responsible for making annual contributions intended to help the participant reach that projected retirement target.

However, it is critical to understand that the target benefit is not guaranteed.

Because the employer’s obligation is limited to making required contributions, rather than guaranteeing the final payout amount, the plan remains classified as a defined contribution plan rather than a defined benefit plan.

Like MPPPs, target benefit pension plans generally cannot invest more than 10% of plan assets in employer stock, helping reduce excessive concentration risk. Additionally, employees typically do not contribute to these plans; they are funded entirely by the employer.

Important Clarification

This is an excellent example of why understanding retirement plan terminology matters.

Although an MPPP is called a “pension plan,” it is still a defined contribution plan, not a defined benefit plan.

The distinction comes down to what the employer is obligated to provide:

Defined contribution plans focus on the amount contributed each year.

Defined benefit plans focus on guaranteeing a specific retirement payout in the future.

With an MPPP, the employer is obligated to contribute a specific amount annually, but there is no guaranteed retirement payout amount. Therefore, the plan remains classified as a defined contribution plan.

Concluding Thoughts

While this may seem like more information than the average person wants to know about retirement plans, understanding the basics of defined contribution plans can significantly improve your ability to evaluate and maximize employer benefits.

Different retirement plans come with different:

Contribution rules

Investment structures

Vesting schedules

Distribution rules

Tax implications

Retirement risks

These differences can have a major impact on your financial health during both your working years and your retirement years.

The better you understand your employer’s retirement offerings, the more effectively you can plan for long-term financial security.

If you ever want more information about the retirement plans available through your employer, your HR department or benefits team can usually provide additional plan documentation and educational resources.

Disclaimer:

The information provided in this blog is for general educational purposes only and should not be construed as tax, legal, or financial advice. Every individual’s situation is unique, and you should consult a qualified tax professional or financial advisor before making decisions based on this content. Akouson Financial and its representatives are not responsible for any actions taken based on the information provided herein.